Commercial Real Estate

in Central Massachusetts

Investment sales, leasing, and development across Worcester and Central MA, with a data-driven edge most brokerages can't match.

Free Property Valuation

Thinking about selling? Tell us where the building is. We respond within one business day.

We fix what's costing you money.

Spencer, MA. Serving Worcester County

and Central New England since 1990.

Know what you own.

Most commercial property owners in Worcester County haven't had their building valued since they bought it. Markets shift. Rents move. A free Broker Opinion of Value from our team gives you a clear picture, built on local comps and thirty-five years of transaction history, not an algorithm.

Request a ValuationFill what's empty.

Every month a commercial space sits vacant, it costs you money. We lease industrial, retail, office, and flex space across eight Central Massachusetts submarkets. Tenant prospecting, competitive positioning, lease negotiation. First showing to signed lease.

Leasing ServicesMove when it's time.

When you're ready to buy or sell commercial property in Central Massachusetts, the deal often starts before the listing goes public. We represent buyers and sellers across Worcester County, and our network means we hear about opportunities first.

Investment Sales

Todd Lornell

Principal & Founder

Collin Mulcahy

President

Michael Murray

Advisor

Faisal Yaseen

Director of IT

Proven Results

Our track record speaks for itself. Here are some of our recent successful transactions and completed deals.

SOLD — OFF MARKET

10 Sheridan Street - Multifamily

10 Sheridan St, Worcester, MA

We closed the off-market sale of this 3-family home at 10 Sheridan Street in Worcester, MA. It never went on the public market. I worked my buyer list, brought in several qualified investors, and the competition on it pushed the price well above our client's expectations.

Need to move a multifamily or commercial property quickly? Give me a call.

Collin Mulcahy

Transaction Lead

SOLD: $795,000

78 Green Hill Parkway - Multifamily

78 Green Hill Pky, Worcester, MA

When 78 Green Hill Parkway closed at $795,000, that put all three buildings in the Green Hill Parkway portfolio under contract and closed: nine units, $2.4 million total, done in three weeks. Buyers are still fighting over well-located Worcester multifamily, and this portfolio shows it.

Thinking about selling your multifamily? Reach out and I'll tell you what it's worth in today's market.

Collin Mulcahy

Transaction Lead

SOLD: $300,000

DOWNTOWN OFFICE CONDO, $200K

415 Main St, Worcester, MA

We sold two office condominium units at 415 Main Street, one of the better-known commercial buildings in downtown Worcester. A local owner-user/investor bought both. That kind of demand for well-located commercial property in Worcester hasn't let up. Every deal has its snags, and this one had its share. When they came up, we worked through them and did what we had to do to close it for our seller clients.

Thinking about buying, selling, or investing in commercial property? The team at LRE will outwork anyone. Call us and we'll tell you what your downtown Worcester property is worth right now.

Collin Mulcahy

Transaction Lead

SOLD: $765,000

74 Green Hill Parkway - Multifamily

74 Green Hill Pky, Worcester, MA

We closed on this 3-unit multifamily at 74 Green Hill Parkway in Worcester, MA. It had a few bumps along the way, but we worked through the negotiations and put together a deal that made sense for everyone. I'm proud of how this one came together. Multifamily investors keep looking at Worcester, and this sale is one more sign of the demand for well-located buildings in the Brittan Square neighborhood.

Thanks to Matthew Czepiel for the work getting this one across the finish line. Thinking about selling your multifamily? Get in touch and I'll tell you what it's worth in today's market.

Collin Mulcahy

Transaction Lead

SOLD: $845,000

82 Green Hill Parkway - Multifamily

82 Green Hill Pky, Worcester, MA

We closed this 3-unit multifamily at 82 Green Hill Parkway in Worcester, MA. My job was to get my seller the right number and a buyer who could actually close, and that's what happened. Worcester multifamily keeps pulling in investors, and a lot of that demand is coming from out of town. Buyers are hunting for well-priced deals like this one.

Thinking about selling your multifamily? Reach out and I'll tell you what it's worth in today's market.

Collin Mulcahy

Transaction Lead

TENANT RETAINED

FULLY LEASED RHODE ISLAND WAREHOUSE

1155 Victory Hwy, Burrillville, RI

We leased this 10,000 SF warehouse to a creditworthy international tenant, and CoStar Group named it a Q2 2025 Quarterly Deals winner. We later extended the lease and locked in a multi-year triple net lease. It is fully leased and producing income now.

Want a fully leased, income-producing building like this one? Call me and I will walk you through it.

Collin Mulcahy

Transaction Lead

8,000+ SF LEASED

CVS-ANCHORED CENTER ON ROUTE 9

133 Main St, Spencer, MA

This one took more than a year of back-and-forth to get across the line, but we closed a lease at our retail listing in Spencer, MA. Dollar Tree Stores is taking over 8,000 SF of end-cap space at Spencer Shoppers' Village. A national retailer in a spot that's easy to see from the road, and it adds real strength to the center.

Deals like this run long and have a lot of moving parts. When it finally comes together for the landlord I represent, the work is worth it. Have space to lease? Let's talk.

Collin Mulcahy

Transaction Lead

6-UNIT MULTIFAMILY SOLD

126 Lincoln Street - Multifamily

126 Lincoln Street, Worcester, MA

We represented the buyer on this 6-unit multifamily asset in Worcester's growing rental market. Thanks to Rich Jenkins, who was a pro throughout and kept the closing on track.

Thinking about getting into multifamily? Give us a call.

Collin Mulcahy

Transaction Lead

RETAIL STRIP LEASED

Sutton Ave - Retail

486 Sutton Ave, Oxford, MA

We leased this retail strip on Sutton Ave in Oxford, MA. The end-cap unit is going to Goswick Eye, who are opening their newest location at this high-visibility, high-traffic intersection in the middle of town. It's an older building that has held a lot of good businesses over the years, and I expect this medical tenant will do the same.

Good tenants come to landlords who are patient. Waiting for the right fit usually pays off over the long run. Have a space you're trying to fill? Give me a call.

Collin Mulcahy

Transaction Lead

FORMER CHERRY VALLEY MILL ON ROUTE 9

Market Leaders

Decades of experience shaping the skyline and community of Central New England.

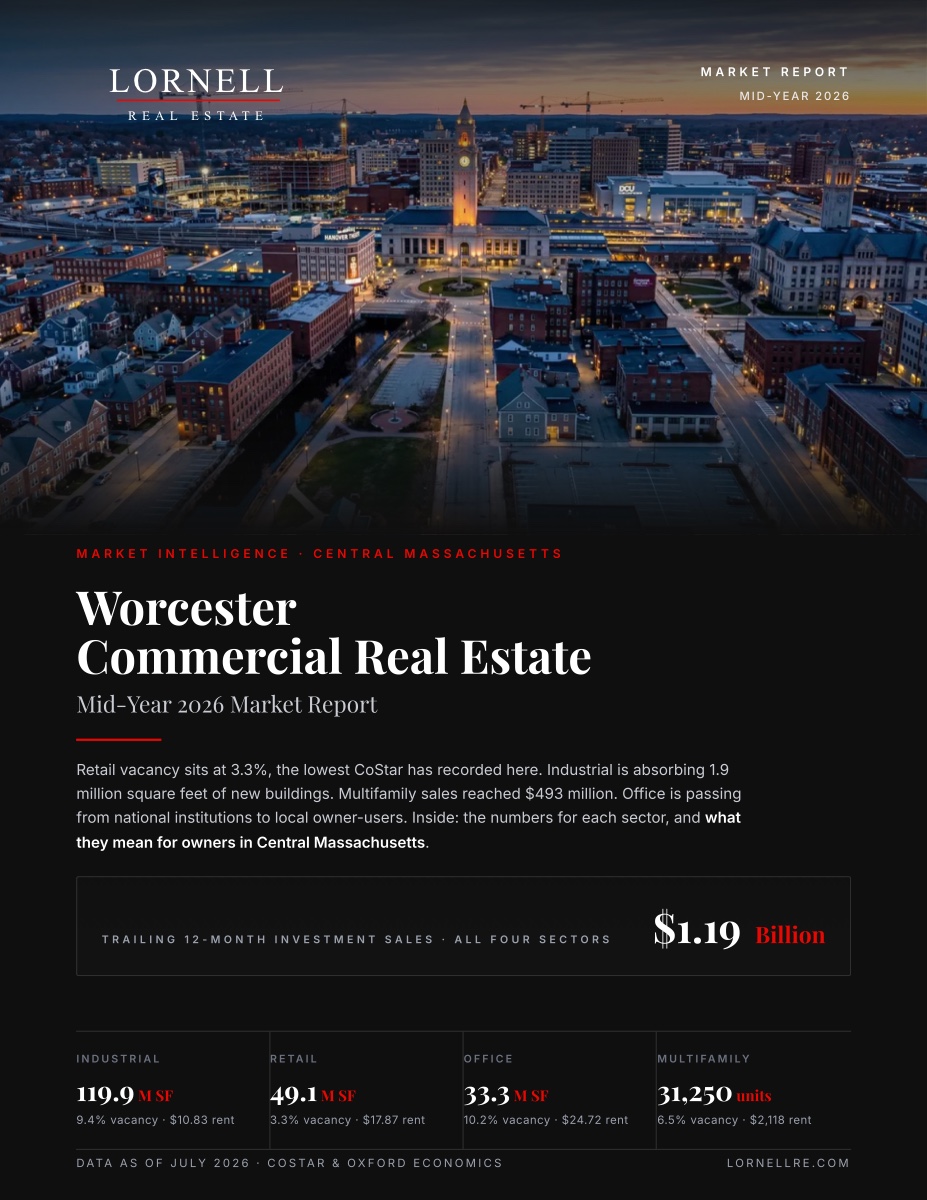

Market Intelligence

Worcester Commercial Real Estate

Mid-Year 2026 Market Report

Eleven pages on the industrial, multifamily, office, and retail markets: submarket vacancy and rents, the headline transactions, cap rates, and the 2026-2030 outlook.

Get the free report by email

Read the Highlights